From Seed to Series B: The Compliance Roadmap Every Fintech Founder Needs (But No One Explains)

Compliance is the trust layer for fintech startups, and treating it as a growth function - not an afterthought - can make or break your journey from Seed to Series B. Here's the challenge: regulatory hurdles, security expectations, and investor demands grow as you scale. Neglecting compliance early often leads to costly fixes later.

This guide breaks down the key compliance steps for fintech founders at each stage:

Automation tools can handle up to 90% of audit tasks, saving time and reducing errors. But compliance isn't just about tools - it's about building trust with enterprise clients, investors, and regulators.

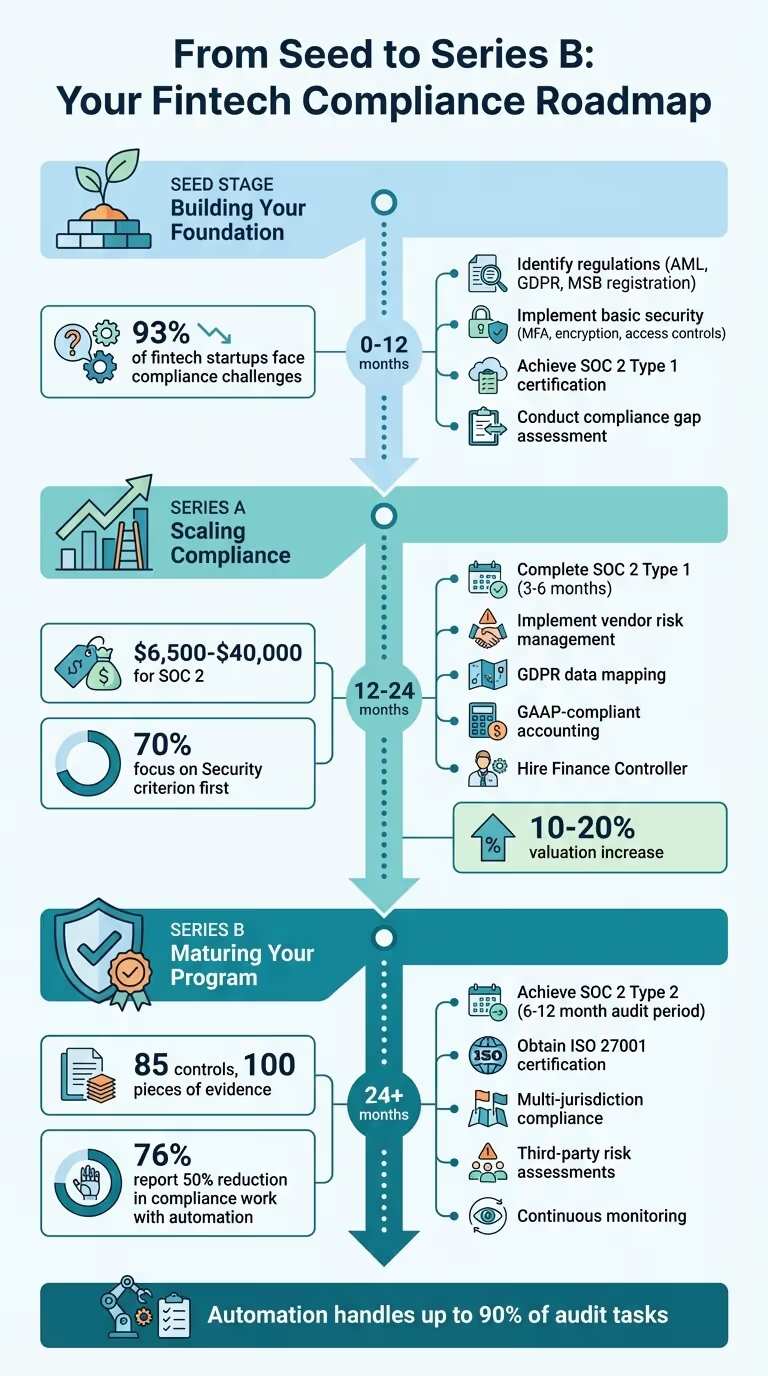

Seed Stage: Building Your Compliance Foundation

At the seed stage, navigating compliance can feel overwhelming - 93% of fintech startups report facing challenges in this area. The solution? Build a foundation that scales with your growth. By embedding compliance into your product architecture early on - what experts call integrated compliance - you can avoid expensive overhauls later. Start by identifying your regulatory requirements, implementing essential security measures, and conducting a gap assessment to solidify your approach.

Identifying Your Regulatory Requirements

The first step is understanding which regulations apply to your business model. For example, if your startup handles money transmission, currency exchange, or cryptocurrency in the U.S., you’ll need to register as a Money Services Business (MSB) with FinCEN. This involves filing Form 107 within 180 days of launching and renewing the registration every two years.

"If your startup deals with money transmission, currency exchange, or cryptocurrency, you'll need to register as a Money Services Business (MSB) with FinCEN." - Rimsha Jalil, Fintech and Compliance Writer

Beyond registration, you'll need a written Anti-Money Laundering (AML) program under the Bank Secrecy Act. This program should include internal controls, a compliance officer, employee training, and independent audits. If your platform handles user data, you’ll also need to address privacy laws like the Gramm-Leach-Bliley Act (GLBA) for financial data, CCPA for California residents, and GDPR for EU citizen data - violations of GDPR can lead to fines of up to 4% of global annual revenue or €20 million, whichever is higher.

Most U.S. states also require a Money Transmitter License. However, many seed-stage fintechs rely on Banking-as-a-Service partnerships to bypass licensing complexities early on. If you’re processing credit card payments, PCI DSS compliance is a must. To simplify this, consider using tokenization or third-party checkout providers.

Another milestone to aim for is SOC 2 Type 1 certification. This evaluates the design of your security controls at a specific point in time and can help build trust with both investors and enterprise customers. Focus on the "Security" category first, as it’s the only required component for initial attestations.

Implementing Basic Security Controls

From day one, prioritize multi-factor authentication (MFA), encrypt data at rest and in transit, and enforce strict access controls for sensitive information. These measures are non-negotiable. Additionally, set up firewalls, document security policies, maintain backup logs, and establish service-level agreements.

Security training shouldn’t stop with your engineering team - every employee needs to understand their role in safeguarding compliance. Automate as much as possible, like hourly checks for misconfigurations, and centralize documentation to streamline audits. For KYC (Know Your Customer) requirements, using third-party identity verification vendors can help automate your Customer Identification Program. Just be sure to monitor for false positives that might block legitimate users.

Running Your First Compliance Gap Assessment

A compliance gap assessment helps you measure your current security posture against the standards you need to meet. Start by mapping your data flows: identify what personal or financial data you collect, where it’s stored, who has access, and how long you retain it. Then compare your existing controls - technical, access-related, and administrative - against the criteria of your chosen compliance framework.

Document any deficiencies and prioritize fixes based on risk level and regulatory requirements. Tackling smaller gaps first can help build momentum without disrupting daily operations. Assign clear ownership of each control to specific team members for accountability. Perform these internal reviews quarterly to catch issues early, before they’re flagged by external auditors or investors.

"For lean startups, try to keep data mapping practical, not academic. Start with the flows that actually drive your business, use tools that won't add friction, and revisit when your product or vendors change." - Evan Rowse, GRC Subject Matter Expert, Vanta

sbb-itb-ec1727d

Series A: Scaling Compliance as You Grow

As you move into Series A, the stakes get higher. Enterprise customers demand proof of strong security practices, and investors expect operational discipline. Around 70% of startups zero in on the Security criterion for their first SOC 2 report, making it a practical goal that doesn’t overburden your team. Plus, companies with solid financial operations often see valuations rise by 10–20% during funding rounds.

Getting SOC 2 Type 1 Certified

Most founders aim to achieve SOC 2 Type 1 certification within 3–6 months of closing their Series A round. Why? It’s often a key to unlocking enterprise sales. SOC 2 Type 1 focuses on evaluating your control design at a single point in time, making it faster to complete than Type 2. While Type 1 typically takes 4–12 weeks, Type 2 can stretch to 6–12 months. The investment is worth it - a single $500,000 enterprise deal can easily cover these costs.

Here’s a breakdown of expenses:

"Security control ownership isn't just about assigning tasks... it's about embedding security into the culture of the organization. When people understand what they're accountable for... compliance stops being a checklist and turns into a shared mission."

– Faisal Khan, GRC Solutions Expert, Vanta

Once you’ve built this SOC 2 foundation, the next step is expanding compliance efforts to address vendor and data privacy risks.

Managing Vendor Risk and GDPR Data Mapping

As your company grows, regulators expect you to take responsibility for your entire supply chain. If one of your vendors experiences a breach, authorities will examine your due diligence process. To manage this risk effectively, categorize vendors based on their level of access and importance:

For GDPR compliance, start by mapping how personal data flows through your organization. Identify data sources, storage locations, and purposes. This process forms the basis of your Record of Processing Activities (RoPA), a requirement under Article 30. Make sure to document the lawful basis for each use of data - whether it’s Consent, Contract, Legal Obligation, or Legitimate Interest. Using automation tools can cut your GDPR compliance workload by up to 50%.

As you shore up your technical and vendor compliance, it’s equally important to strengthen your financial operations.

Setting Up Financial Compliance Practices

Series A is the time to shift from basic cash-basis accounting to GAAP-compliant accrual accounting. You’ll also need to hire your first full-time Financial Controller or Finance Manager, ideally someone with ACA, ACCA, or CIMA qualifications. Expect to pay $65,000–$95,000 annually, plus equity. This hire will handle month-end close and investor reporting, aiming to reduce close times to 5–10 days compared to the 10–15 days typical at the Seed stage.

To streamline financial processes:

Finally, prepare for your first external audit. Start a "pre-audit cleanup" 2–3 months before your fiscal year-end. This effort can cut external audit fees by 20–30%. For companies with $1 million to $5 million in revenue, audit costs typically range from $15,000 to $30,000.

Series B: Maturing Your Compliance Program

By the time your startup reaches Series B, your compliance program needs to evolve from simply responding to issues to anticipating and preventing them. Enterprise customers and institutional investors will expect continuous proof that your controls are not only in place but also functioning effectively. Building on the groundwork laid during Series A, this phase emphasizes maintaining operational excellence and managing risks more effectively. A mature compliance program at this stage is key to retaining investor confidence and supporting global expansion.

Obtaining SOC 2 Type 2 and ISO 27001 Certifications

SOC 2 Type 2 is the logical next step after achieving SOC 2 Type 1. While Type 1 confirms that your controls are well-designed at a specific point in time, Type 2 goes further by verifying that these controls are effective over a sustained period, usually 6 to 12 months. Auditors will typically evaluate about 85 controls and request around 100 pieces of evidence.

To meet Series B requirements, continuous evidence collection becomes essential. This means implementing systems that automatically capture audit logs, perform access reviews, and document incident response tests. Automation can be a game-changer - 76% of companies using automated platforms report cutting compliance-related work by at least half.

ISO 27001 takes things a step further. Unlike SOC 2, which is attestational, ISO 27001 is a formal certification that requires an Information Security Management System (ISMS) and a plan for ongoing improvement. It’s particularly valuable for companies eyeing international markets, especially in Europe and Asia-Pacific. The investment can be well worth it, considering that data breaches cost an average of $220,000 more when non-compliance is involved.

These certifications ensure your internal controls are robust, but don’t overlook the importance of managing external risks through structured assessments of third-party vendors.

Conducting Third-Party Risk and Privacy Impact Assessments

As your company scales, managing third-party risks becomes increasingly important. Data shows that 62% of breaches involve third-party vendors, and nearly every organization (98%) has at least one vendor that has experienced a breach.

To address this, adopt a tiered vendor risk model that applies varying levels of scrutiny based on the risk posed by each vendor:

For SOC 2 compliance, ensure vendors provide formal privacy commitments and establish incident notification protocols, typically within 24 to 72 hours. Maintain a centralized vendor register that tracks each vendor’s risk tier, data access level, Data Processing Agreement (DPA) status, and the next scheduled assessment. For Tier 1 and Tier 2 vendors, negotiate audit rights into contracts and implement a formal offboarding process to revoke access and obtain written data deletion confirmations when the relationship ends.

"Your organization's security is only as strong as your weakest vendor." – Vision Compliance

Handling Multi-Jurisdiction Compliance

Expanding into international markets introduces a maze of regulatory requirements. In 2023 alone, over 800 new financial regulations were introduced globally, and AML-related fines exceeded $5 billion in 2024. The best way to handle this complexity is by designing modular compliance processes - breaking them into flexible units that can be quickly adapted for new markets.

Begin with a three-step framework: identify your business activities, analyze target markets, and map out the relevant regulatory requirements. Use control cross-mapping to minimize redundant work. For example, evidence from ISO 27001 can often satisfy requirements for SOC 2 or even the EU AI Act.

Companies like Sitoo have shown how effective this approach can be. By building custom compliance frameworks, they achieved compliance in over 20 countries, significantly shortening sales cycles. Similarly, Wise (formerly TransferWise) managed global scaling by first obtaining a license in Estonia before securing one in the UK to anchor their international operations.

At this stage, hiring regional compliance experts can be a smart move. For example, you might need an AI Compliance Lead to handle EU AI Act requirements or a Partner Compliance Lead to oversee Bank-as-a-Service (BaaS) relationships. If your company processes large volumes of sensitive data in the EU, appointing a Data Protection Officer (DPO) is not just a good idea - it’s legally required.

Key Compliance Frameworks for Fintech Companies

For fintech companies, compliance frameworks like SOC 2, ISO 27001, and GDPR are essential pillars for managing regulatory hurdles and scaling effectively. These frameworks not only align with growth stages but also meet investor expectations and market demands.

SOC 2 is a cornerstone for North American B2B operations. It evaluates five Trust Services Criteria: security, availability, processing integrity, confidentiality, and privacy. Early-stage fintechs (Seed or Series A) typically pursue SOC 2 Type 1, which assesses the design of their controls at a specific point in time. By Series B, SOC 2 Type 2 becomes a necessity, showcasing the operational effectiveness of these controls over a 3–12 month period. Automation can significantly speed up this process, cutting the average completion time to 3.1 months compared to 6.8 months for manual approaches.

ISO 27001 is crucial for fintechs looking to expand internationally, particularly in Europe or Asia-Pacific. Unlike SOC 2, ISO 27001 involves formal certification of an Information Security Management System (ISMS) and is highly regarded by large financial institutions. This certification helps establish credibility on a global scale and is often a prerequisite for high-stakes partnerships.

For fintechs handling EU/EEA data, GDPR compliance is non-negotiable. Non-compliance risks fines of up to €20 million or 4% of global revenue. Startups should focus on practical data mapping, prioritizing the flows critical to their operations. Many rely on "Consent" for marketing activities and "Contract" for core service delivery. Automation platforms can handle up to 50% of GDPR compliance tasks, streamlining this complex process.

"Compliance is the trust layer – and the leaders who treat it like a growth function are winning." – Darren Vorster

Common Compliance Challenges

Compliance costs are frequently underestimated. On average, startups anticipate spending $35,000 but often face actual costs of $84,000 - 2.4 times higher than expected. Additionally, 34% of companies fail their first readiness assessment, usually due to access control issues like shared credentials or missing multi-factor authentication. A smart approach to compliance involves cross-mapping controls between frameworks. For instance, evidence collected for SOC 2 can often satisfy ISO 27001 requirements, saving both time and resources.

Controls for Payments and Data Security

The fintech sector demands specialized security measures, particularly for payment systems and sensitive customer data. Compliance frameworks provide clear guidelines for these areas:

In addition to these frameworks, U.S.-based fintechs must navigate regulations like KYC/KYB (identity verification), AML (anti-money laundering), OFAC (sanctions screening), and UDAAP (consumer protection). For example, under the Truth in Lending Act (TILA), employees cannot be held liable for more than $50 for unauthorized credit card use. Emerging regulations, such as the EU AI Act and the CFPB's Rule 1033, are also reshaping requirements, particularly for AI-driven credit scoring and fraud detection.

Maintaining Continuous Monitoring and Remediation

Traditional audits often involve last-minute evidence collection, but continuous monitoring ensures year-round readiness. Automated systems now replace manual spreadsheets and quarterly tasks with hourly checks of security settings. These platforms integrate with HR systems, cloud infrastructure, and development tools to automatically verify controls like multifactor authentication, encryption, and access permissions. As a result, 78% of fintechs use compliance automation platforms, completing certifications 40% faster than those relying on manual processes. Automation can handle up to 90% of audit tasks.

However, automation alone has its limits. Traditional GRC tools track compliance tasks but don’t execute them. Cycore's AI-human hybrid model fills this gap by continuously collecting evidence, identifying issues, and assisting with remediation - all while freeing up experts to focus on strategy and risk management. This approach minimizes operational disruptions, speeds up deal closures, and ensures audit readiness year-round.

To sustain effective monitoring, establish a testing cadence: test critical systems monthly and key controls quarterly to avoid control drift. Assigning control ownership across teams embeds security into your company culture and ensures accountability. This distributed model, combined with automated tools and expert oversight, creates a scalable compliance program that evolves with your business.

Conclusion

Navigating compliance from Seed to Series B can feel like a maze, but founders who weave it into their growth plans often find they can close deals faster and secure funding with greater ease. Each growth stage brings its own set of requirements: foundational controls and data mapping at Seed, SOC 2 Type 1 and vendor risk management at Series A, and SOC 2 Type 2 and ISO 27001 at Series B to showcase operational maturity.

Automation offers a game-changing advantage, with companies able to handle up to 90% of audit tasks without manual effort. Still, startups spend an average of 4,300 hours annually on compliance, and in 2024, 36% of companies faced cyberattacks costing at least $1 million. Taking a proactive approach to compliance doesn’t just protect you - it shortens sales cycles, boosts revenue, and builds trust with investors.

"The divide in 2026 isn't product. It's trust. Compliance is the trust layer – and the leaders who treat it like a growth function are winning." – Darren Vorster

This highlights the importance of treating compliance as more than a checklist - it’s a growth enabler. That’s where we come in. Unlike traditional GRC tools that merely track tasks, Cycore’s AI-human hybrid model actively executes them. We integrate with your team to design a security program tailored to your needs, while handling evidence collection, policy creation, control implementation, and audit facilitation. Our AI tools monitor your environment in real time, spot gaps, and help resolve them, while our experts focus on strategy and risk management to keep you audit-ready at all times.

Whether you're gearing up for your first SOC 2 audit or scaling your operations across new markets, Cycore serves as your fractional security, compliance, and privacy team, so you can concentrate on what matters most - growing your fintech.

FAQs

What compliance work should I do before writing any code?

Before diving into coding, take the time to understand the compliance frameworks that apply to your business. Conduct internal audits to identify gaps, and establish controls to safeguard data security and privacy. These steps lay the groundwork for regulatory readiness and can save your company from expensive rework as it scales.

When should I choose SOC 2 Type 1 vs. SOC 2 Type 2?

Choose SOC 2 Type 1 if you need a faster and more affordable way to evaluate the design of your controls at a single point in time. This option works well when you're addressing immediate requests from clients or investors.

On the other hand, go with SOC 2 Type 2 for a deeper assessment of how effectively your controls operate over a period of 3 to 12 months. This approach is better suited for building lasting trust and supporting ongoing growth.

Do I need an MSB registration or money transmitter licenses to launch?

If your fintech manages or transfers money on behalf of others, you’ll probably need to register as a Money Services Business (MSB) with FinCEN, obtain the necessary money transmitter licenses, and set up Anti-Money Laundering (AML) programs. Skipping these steps can result in serious federal penalties. It’s crucial to fully understand these obligations before launching to stay compliant and steer clear of legal trouble.

Related Blog Posts

- 2025 Security Compliance Requirements for Fintech

- What Is Compliance Mapping?

- Risk Assessment Steps for Regulatory Changes

- The Real Cost of Failing a SOC 2 Audit: What Fintech Companies Lose Beyond the Certification

{"@context":"https://schema.org","@type":"FAQPage","mainEntity":[{"@type":"Question","name":"What compliance work should I do before writing any code?","acceptedAnswer":{"@type":"Answer","text":"<p>Before diving into coding, take the time to understand the <strong>compliance frameworks</strong> that apply to your business. Conduct <strong>internal audits</strong> to identify gaps, and establish controls to safeguard data security and privacy. These steps lay the groundwork for regulatory readiness and can save your company from expensive rework as it scales.</p>"}},{"@type":"Question","name":"When should I choose SOC 2 Type 1 vs. SOC 2 Type 2?","acceptedAnswer":{"@type":"Answer","text":"<p>Choose <strong>SOC 2 Type 1</strong> if you need a faster and more affordable way to evaluate the design of your controls at a single point in time. This option works well when you're addressing immediate requests from clients or investors.</p> <p>On the other hand, go with <strong>SOC 2 Type 2</strong> for a deeper assessment of how effectively your controls operate over a period of 3 to 12 months. This approach is better suited for building lasting trust and supporting ongoing growth.</p>"}},{"@type":"Question","name":"Do I need an MSB registration or money transmitter licenses to launch?","acceptedAnswer":{"@type":"Answer","text":"<p>If your fintech manages or transfers money on behalf of others, you’ll probably need to register as a <strong>Money Services Business (MSB)</strong> with FinCEN, obtain the necessary <strong>money transmitter licenses</strong>, and set up <strong>Anti-Money Laundering (AML)</strong> programs. Skipping these steps can result in serious federal penalties. It’s crucial to fully understand these obligations before launching to stay compliant and steer clear of legal trouble.</p>"}}]}